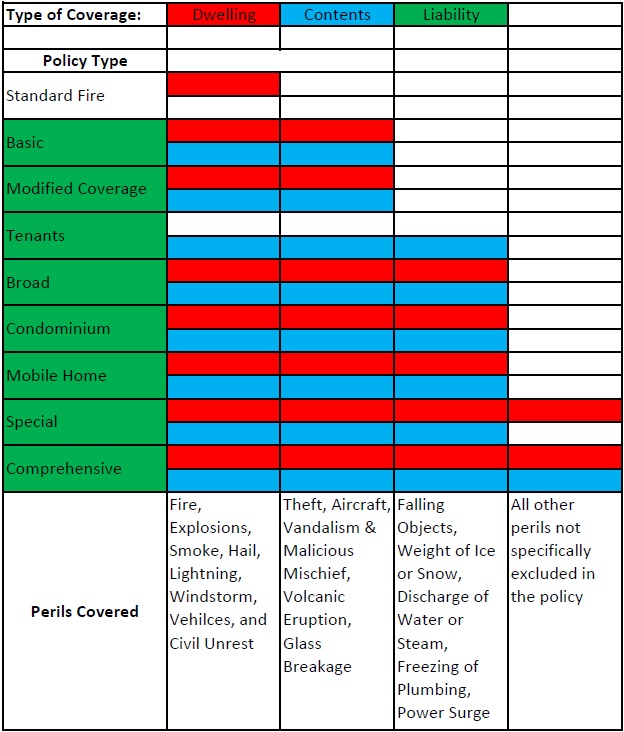

There are nine different types of homeowners policies which all provide different levels of coverage. They are each listed below with a brief description.

Standard Fire Form

A form that provides coverage on a home against fire, smoke, windstorm, hail, lightning, explosion, vehicles, and civil unrest. It does not cover your personal property, personal liability, or medical expenses. It is the type of policy your mortgage lender will buy for you if you let your homeowner policy lapse.

A form that provides coverage on a home against fire, smoke, windstorm, hail, lightning, explosion, vehicles, and civil unrest. It does not cover your personal property, personal liability, or medical expenses. It is the type of policy your mortgage lender will buy for you if you let your homeowner policy lapse.

Basic Form

A basic policy form that provides coverage on a home against 11 listed perils; contents are generally included in this type of coverage, but must be explicitly enumerated. Perils not covered include floods, earthquakes. Most states no longer offer this type of coverage.

A basic policy form that provides coverage on a home against 11 listed perils; contents are generally included in this type of coverage, but must be explicitly enumerated. Perils not covered include floods, earthquakes. Most states no longer offer this type of coverage.

Broad Form

A more advanced form that provides coverage on a home against 16 listed perils (including all 11 on the Basic Form). The coverage is usually a "named perils" policy, which lists the events that would be covered.

A more advanced form that provides coverage on a home against 16 listed perils (including all 11 on the Basic Form). The coverage is usually a "named perils" policy, which lists the events that would be covered.

Special Form

The typical, most comprehensive form used for single-family homes. The policy provides "open peril" coverage on the home with some perils excluded, such as earthquake and flood. Contents are covered on a named peril basis. (Note: "open peril" means all perils not specifically excluded in the policy.)

The typical, most comprehensive form used for single-family homes. The policy provides "open peril" coverage on the home with some perils excluded, such as earthquake and flood. Contents are covered on a named peril basis. (Note: "open peril" means all perils not specifically excluded in the policy.)

Tenants Form

The Contents Broad, or Tenants, form is for renters. It covers personal property against the same perils as the contents portion of the Broad Form. An Tenants Form generally also includes liability coverage for personal injury or property damage inflicted on others.

The Contents Broad, or Tenants, form is for renters. It covers personal property against the same perils as the contents portion of the Broad Form. An Tenants Form generally also includes liability coverage for personal injury or property damage inflicted on others.

Comprehensive Form

Covers the same as Special Form plus more. On this policy the contents are covered on an open peril basis, therefore as long as the cause of loss is not specifically excluded in the policy it will be covered for that cause of loss.

Covers the same as Special Form plus more. On this policy the contents are covered on an open peril basis, therefore as long as the cause of loss is not specifically excluded in the policy it will be covered for that cause of loss.

Unit-Owners Form

The form for condominium owners. It insures your personal property, your walls, floors and ceiling against all of the perils in the Broad Form.

The form for condominium owners. It insures your personal property, your walls, floors and ceiling against all of the perils in the Broad Form.

Mobile Home Form

This policy is essentially the same as the Special Form policy, but it provides protection for mobile and manufactured homes.

This policy is essentially the same as the Special Form policy, but it provides protection for mobile and manufactured homes.

Modified Coverage Form

The form is for the owner-occupied older home whose replacement cost far exceeds the property's market value. It provides coverage on the dwelling and personal property similar to the Broad Form, but it also includes certain restrictions on valuation of losses. In many areas, it is no longer available.

The form is for the owner-occupied older home whose replacement cost far exceeds the property's market value. It provides coverage on the dwelling and personal property similar to the Broad Form, but it also includes certain restrictions on valuation of losses. In many areas, it is no longer available.

The covered perils are explained further by the table below:

As you can see, all policies provide liability protection except a Standard Fire policy. The levels of protection, however, vary from one to the next.