Social Security

Social Security benefits are determined by a formula based on earnings. Nearly 90% of all employed persons are covered by Social Security and pay Social Security taxes. Employees pay 50% of the employment tax. Self-employed persons pay 100% of the tax. The Social Security Administration is responsible for administering benefits and collecting premiums.

Types of Benefits

- Monthly retirement benefits for retired workers at least age 62

- Monthly benefits for spouses of retired workers

- Monthly survivor benefits for the spouse and certain other survivors of deceased workers

- Monthly disability benefits for disabled workers and their dependents

- A modest lump-sum death benefit payable at a worker’s death

Eligibility for Social Security

Most workers are covered under Social Security, including common-law employers and employees, most self-employed persons, Armed Forces personnel, and employees of nonprofit organizations.

The main excluded worker groups are railroad workers and federal employees hired before 1984. Federal employees hired after 1984 are covered. Railroad workers contribute to their own railroad retirement system.

In addition, employees of state and local governments are not covered unless the government entity has entered into an agreement with the Social Security Administration or does not have a retirement program.

The main excluded worker groups are railroad workers and federal employees hired before 1984. Federal employees hired after 1984 are covered. Railroad workers contribute to their own railroad retirement system.

In addition, employees of state and local governments are not covered unless the government entity has entered into an agreement with the Social Security Administration or does not have a retirement program.

Primary Insurance Amount (PIA)

Social Security benefits are expressed as a percentage of the primary insurance amount (PIA). The PIA for a worker is based on the average level of earnings of that worker and is updated and published annually in tables by the federal government. Most types of Social Security benefits are some percentage of the PIA as set for the year for the worker’s earnings level. You can find your PIA at the Social Security Administration's website here.

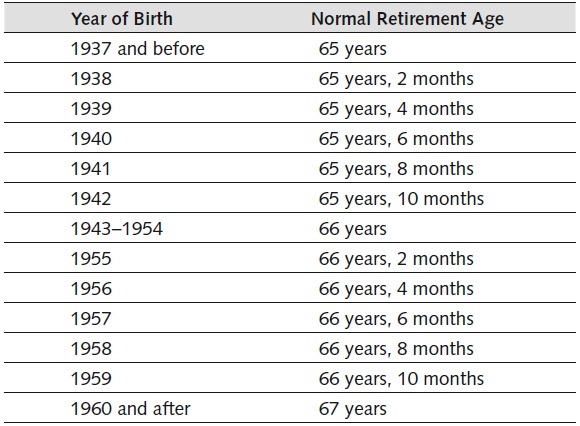

Normal Retirement Age

To receive full Social Security retirement benefits, a person must wait until normal retirement age. If benefits are taken before this age, the monthly benefit amount is reduced.

The Social Security normal retirement age is currently 65. It will gradually increase to age 67 in accordance with the following table.

The Social Security normal retirement age is currently 65. It will gradually increase to age 67 in accordance with the following table.

Dual Benefits

Often a person is eligible to receive more than one Social Security benefit. For example, a spouse who has reached age 65 may be eligible to receive a retirement benefit based on her own earnings and also a benefit based on her late husband’s earnings. In these cases, the person is entitled to receive only the larger of the two benefit amounts instead of both amounts.

Retirement Earnings Limit

Once a Social Security retiree reaches normal retirement age, there is no restriction on the amount the retiree may earn from employment (or self-employment) without losing Social Security benefits. Retirees age 64 and under may earn only up to a certain amount without a reduction in benefits. One earnings limit applies to retirees who have not yet reached their normal retirement age, and a modified limit applies in the year an individual reaches normal retirement age. The dollar amounts are indexed to inflation and change annually.

For 2010, for example, a retiree who has not yet reached normal retirement age would face a reduction in retirement benefits of $1 for every $2 earned beyond $14,160. In the year an individual reaches normal retirement age, $1 in benefits will be deducted for every $3 earned in excess of $37,680 (the limit for 2010).

For 2010, for example, a retiree who has not yet reached normal retirement age would face a reduction in retirement benefits of $1 for every $2 earned beyond $14,160. In the year an individual reaches normal retirement age, $1 in benefits will be deducted for every $3 earned in excess of $37,680 (the limit for 2010).

Click each link below to learn more.